Introduction: A New Era for Private Capital Allocation

Private markets are undergoing a fundamental shift. Traditional exits through IPOs and acquisitions have slowed dramatically. IPOs in the U.S. nearly dried up in 2024 and 2025, leaving billions in unrealized gains locked inside portfolios.

In response, allocators are turning to innovative liquidity solutions. Venture secondaries and GP-led continuation funds, once considered niche, are now permanent fixtures in private capital markets. They are changing the way capital is recycled, risk is managed, and returns are realized.

For allocators, understanding these tools is no longer optional. They represent the next frontier of private capital allocation.

The Rise of Venture Secondaries

Venture secondaries allow investors, founders, or LPs to sell existing stakes in private companies or funds, providing liquidity without waiting for an IPO or acquisition . In a market defined by an exit drought, secondaries have become a vital pressure valve.

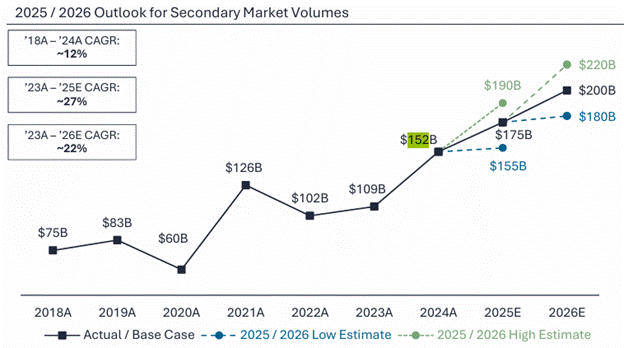

● According to Lazar, Global venture secondary deal volume hit $152 billion in 2024, up 39% year-over-year.

● 2025 is on pace to surpass that record, with analysts projecting the market could exceed $175 billion this year.

Source: Lazard 2024 Secondary Market Report

What makes this trend compelling is not just size but also function. For allocators, secondaries offer a counter-cyclical entry point: they can buy into companies or funds at a discount when others are selling for liquidity.

Continuation Funds and GP-Led Deals

A continuation fund allows a general partner (GP) to transfer one or more portfolio companies from an existing fund into a new vehicle, giving LPs the choice to cash out or roll over .

Once stigmatized, GP-led transactions are now mainstream:

● GP-led deals grew from <20% of secondary volume before 2016 to nearly 50% by 2023–2024.

● According to Bennet Jones, 87% of GP-led deals in 2024 were continuation funds.

● Blue-chip VCs like Lightspeed and Insight Partners launched continuation vehicles in 2024, signaling adoption across venture capital.

For allocators, continuation funds represent direct access to proven “winner” assets with optionality: take liquidity today or stay invested alongside the GP.

Why Allocators Should Care

Allocators ranging from pensions and endowments to family offices and wealth managers are actively engaging with these structures. The benefits are significant:

● Liquidity and flexibility: Unlock capital when portfolios are overallocated or rebalance positions.

● Diversification and shorter durations: Gain exposure to seasoned portfolios and mitigate blind pool risk.

● Discounted access to high-quality assets: Secondary stakes often clear below NAV (12–30% discounts have been common in recent years according to Institutional Investor).

● Competitive returns with lower downside: Secondary funds have historically outperformed buyout and venture funds on a risk-adjusted basis, with 95% avoiding capital loss across vintages 2000–2019.

However, allocators must also navigate challenges: valuation opacity, information asymmetry, illiquidity, and governance risks in GP-led deals . Proper diligence, fairness opinions, and alignment of GP incentives are essential.

The Market Outlook

The secondary market is scaling rapidly:

● Global secondary volume reached $160 billion in 2024, up 41% year-over-year.

● Forecasts suggest it could exceed $200 billion annually in the next two years.

● Blackstone projects the market may grow to $400 billion by 2030.

GP-led deals are expected to dominate, with continuation funds projected to represent up to 20% of all GP exits . Meanwhile, allocators themselves are fueling this growth: public pensions were the most active sellers in early 2024, accounting for 33% of secondary volume.

In parallel, new participants are entering the market, from sovereign wealth funds to retail investors through feeder vehicles, broadening both demand and liquidity.

The Finalis Edge

As allocators navigate this evolving frontier, platforms like Finalis are emerging as key enablers. Finalis connects allocators with curated deal flow from over 850 licensed independent bankers across 1,500+ active transactions.

Through its AI-powered platform, Finalis provides:

● Curated deal access to secondary stakes and continuation vehicles otherwise difficult to source.

● Trusted compliance under a FINRA-regulated umbrella, reducing risk when engaging with independent bankers.

● Smarter deal intelligence through technology and network effects that streamline discovery and execution.

For allocators, this means access to differentiated deal flow with institutional-grade oversight, an edge in a competitive market.

Conclusion: The Next Frontier Is Already Here

Venture secondaries and continuation funds are no longer side plays. They are central to how private capital is being allocated in 2025 and beyond. For allocators, the message is clear: integrating these strategies is no longer about innovation. It is about staying relevant.

Those who embrace this shift will gain liquidity options, portfolio flexibility, and potentially superior returns. Those who ignore it risk being left behind.

At Finalis, our Capital Allocators Program helps investors access these opportunities efficiently and with confidence. As the frontier of private capital expands, we are here to connect you with the deals, compliance, and intelligence to navigate it successfully.