Introduction

Private markets have undergone significant changes over the past five years.

Despite a slowdown in dealmaking and market activity since the 2021 highs, more investors are looking to get into private markets every year, helping the asset class grow at an unprecedented pace.

In our last report, we covered what led to the slowdown in dealmaking since 2021, and here we will cover the trends that have defined the past half decade, and sectors that have performed well between 2020 and 2025.

Several strategies have seen increased popularity: private credit has boomed, search funds have seen greater usage, and SPAC mania has come and gone.

Some sectors have seen increased investment, especially in tech and healthcare, as investors look for new opportunities for outsized returns.

As private markets reach record value, and dealmaking activity thaws over the next couple of years, there are many opportunities available for allocating capital.

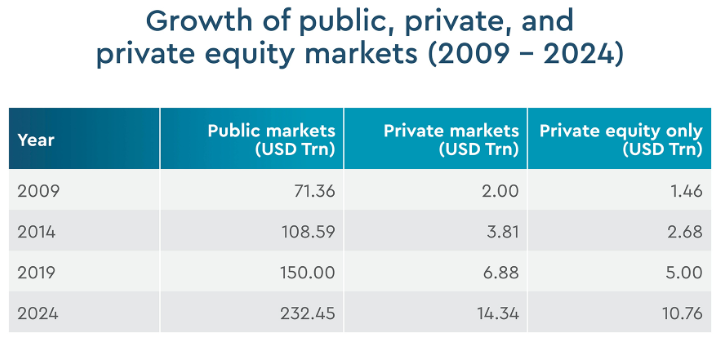

Overall Private Market Growth

A defining characteristic of private markets over the past 5 years has been its explosive growth in net value.

Between 2019 and 2024, the overall total value of private markets more than doubled, from $6.88 trillion to $14.24 trillion:

Source: Ocorian

This growth outpaced that of public markets, underscoring increased interest in alternative assets by investors.

Interest continues to grow, a 2025 study by Adams Street found that 85% of LPs expect private markets to outperform public markets over the long run.

Private Credit Booms

Private credit has been the strongest performing asset in private markets since 2021. And, private credit AUM reached a record $1.6 trillion by the end of 2023.

Amid high-interest rates, access to private credit was a major asset for small-mid sized businesses who found it difficult to meet their needs through traditional banks, especially as banks pull back from corporate lending overall. Today, banks only provide about 30% of corporate loans, versus 70% in 1982.

As a result private credit has become a major category of overall borrowing, worth over $1 trillion as of 2025:

Source: J.P. Morgan

The growth of private equity has been consequential to the growth of private credit, as in about 70% of deals, the borrowing company is backed by a private equity firm.

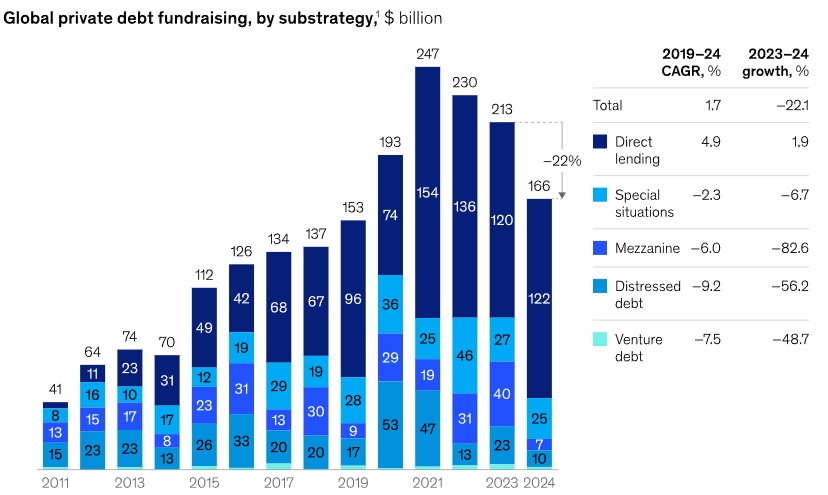

While private debt fundraising fell by 22% in 2024, the sector remained fairly stable following 2021 euphoria compared to other areas of capital markets:

Source: McKinsey

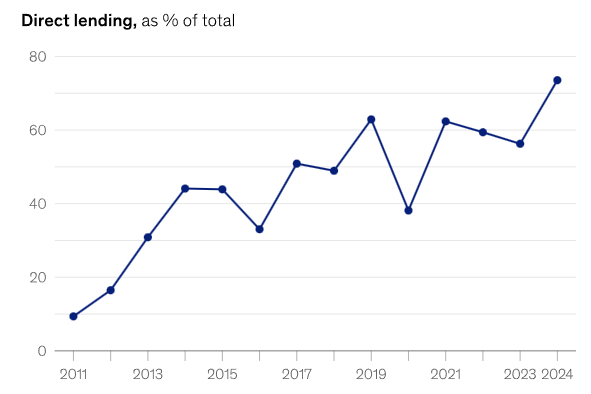

Direct lending has played a major role in keeping the sector steady through the 2022 slowdown, and now encompasses a large portion of private debt fundraising:

Source: McKinsey

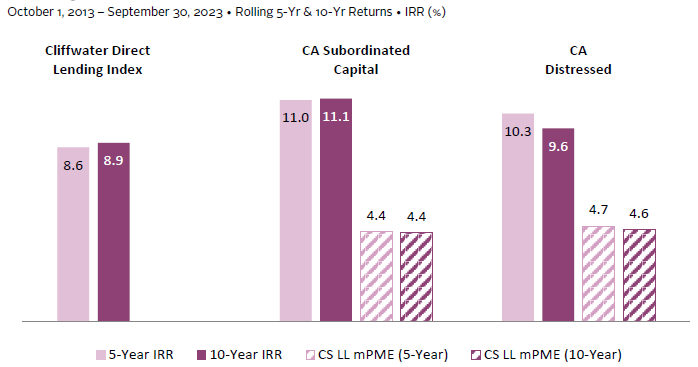

Long-term-returns on private capital funds have also been very compelling, in some cases beating the public market:

Source: Cambridge Associates

Overall, the increasing share of private credit in private markets has helped buoy investors and companies during a period of slower dealmaking and higher borrowing rates, aiding its impressive activity and returns over the past 5 years. Only time will tell if it remains a mainstay in private markets, but as it becomes an increasingly larger share of alternatives, activity should remain strong.

Secondary Markets

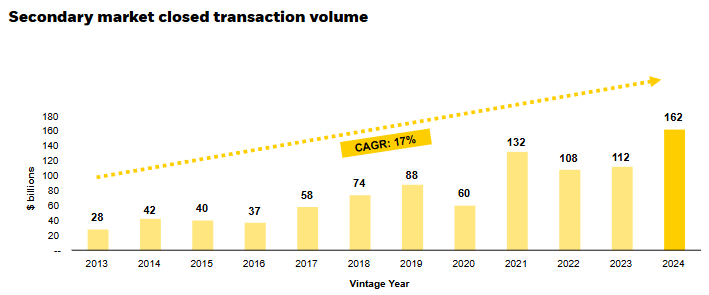

Secondary market transaction value has grown significantly in the past 5 years and 2024 represented a record year.

Total secondaries exit value grew from $60 billion in 2020 to $162 billion in 2024:

Source: Blackrock

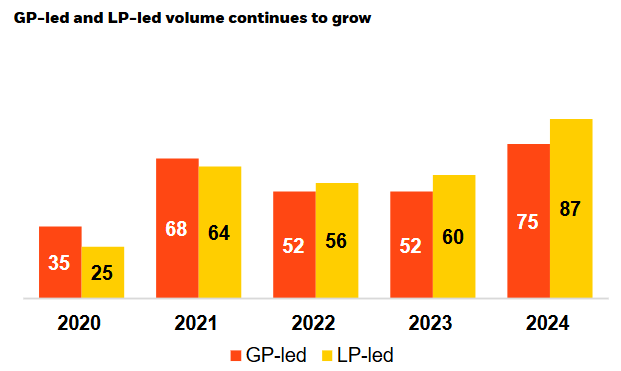

The secondary market has grown for both GP-led and LP-led transactions. GP-led secondary transactions grew from $35 billion in 2020 to $75 billion in 2024. LP-led secondary transactions saw slightly greater growth, from $25 billion in 2020 to $87 billion in 2024:

Source: Blackrock

Following the 2021 activity highs, secondary transaction volume greatly outpaced both M&A and IPOs:

Source: Blackrock

Overall, as dealmaking slowed, fund managers and allocators got creative, and secondaries provided exit opportunities outside of traditional routes like M&A and IPOs. Big secondary deals this year show more to come, including from Yale’s endowment and New York City’s pension fund.

Search Funds Increase in Popularity

While search funds have existed for a few decades, they did not begin to reach mainstream popularity until recently.

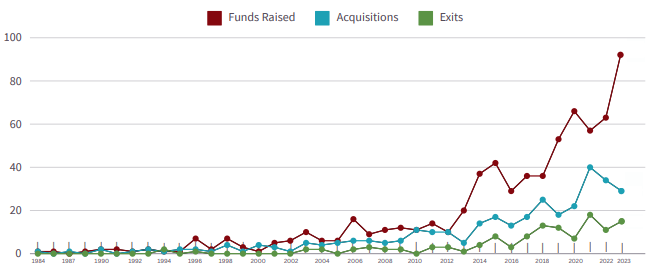

Stanford’s search fund study shows a massive surge in search funds raised in the past few years, with a record 94 in 2023:

Source: Stanford

Over the past 5 years, the gap between raises and acquisitions was at its lowest in 2021, commensurate with increased market activity.

As market activity began to slow, so did acquisitions made by funds. While exits saw a slight decline during the 2022 slowdown, they saw a recovery in 2023.

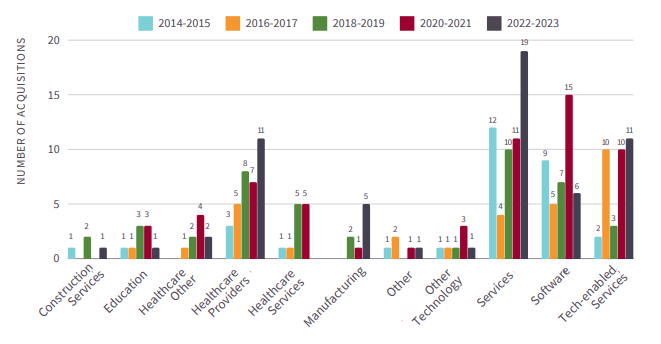

The industries search funds operate in have also changed slightly in the past 5 years, with a greater focus placed on services and healthcare businesses:

Source: Stanford

Software-based searchers peaked during 2020-2021, before seeing a sharp decline in 2022-2023.

The average age of searchers has declined, with 79% being 35 or younger for funds launched between 2022-2023. The study noted that this was due to a rise in searchers coming straight out of undergraduate business school, rather than MBA recipients.

The internal return rate for the 2024 study was 35.1%, slightly down from 35.3% in the 2022 study. And, return-on-investment decreased from 5.2x in 2022 to 4.5x in 2024.

However, returns have remained very attractive despite slower exits, especially when compared to other asset classes.

Overall, with search funds seeing record raises even past 2021 market activity highs, search funds have been a very popular option for investors from 2020-2025. Those that have exited have seen very attractive returns.

As the job market becomes more difficult for undergraduate business and MBA graduates, search funds could become attractive options for those coming from top-tier universities.

SPAC Mania

Similar to search funds, special-purpose-acquisition-companies have been around for a while, but saw increased popularity over the past 5 years, notably through 2020-2021.

During the 2020-2021 market euphoria, SPACs became a popular way for private equity and venture funds to exit companies.

In 2019, 59 SPACs were created, with $13 billion total invested. By 2020, this exploded to 247 created, with $80 billion total invested, accounting for over half of new publicly-listed companies.

In Q1 2021 it reached peak fever, with 295 SPACs created, and $96 billion invested during that quarter alone.

This created major exit opportunities for fund managers and allocators, as the faster exit of a SPAC was more attractive than a traditional IPO.

However, almost just as quickly as it exploded, the trend fizzled out. A main contributor to the decline was the public market slowdown, which affected nearly all capital markets.

Overall, while the trend eventually fizzled out, the SPAC craze showed the interest of retail investors to get in on private companies. While SPACs may not ever return to their 2020-2021 activity, they did plant a seed for growing interest in access to private assets by a wider range of investors.

High-Performing Sectors

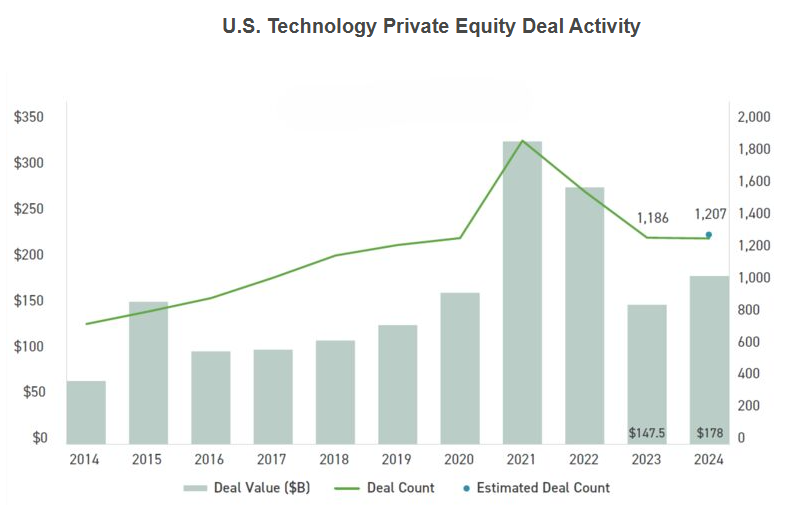

From 2019-2024, the technology industry saw some of the greatest growth in private equity deal activity.

Between 2020 and 2021, deal value doubled from ~$150 billion to over $300 billion:

Source: Cherry Bekaert

While deal value fell sharply by 2023 following the dealmaking slowdown, deal count stayed relatively stable, and value remained above pre-pandemic levels, underscoring continued interest in the sector.

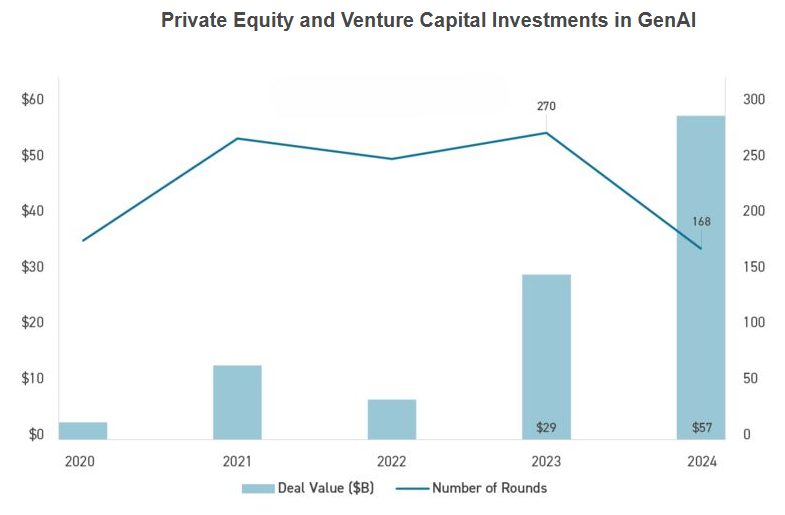

As AI becomes more engrained in day-to-day workflows, investors are looking for ways to get in on the growth.

Private equity and venture capital investments in GenAI ballooned from 2020 to 2024, with deal value reaching $57 billion in 2024:

Source: Cherry Bakaert

70% of GPs expect an increase in tech deals throughout 2025, according to a recent survey by Cherry Bekaert, showing big opportunities ahead.

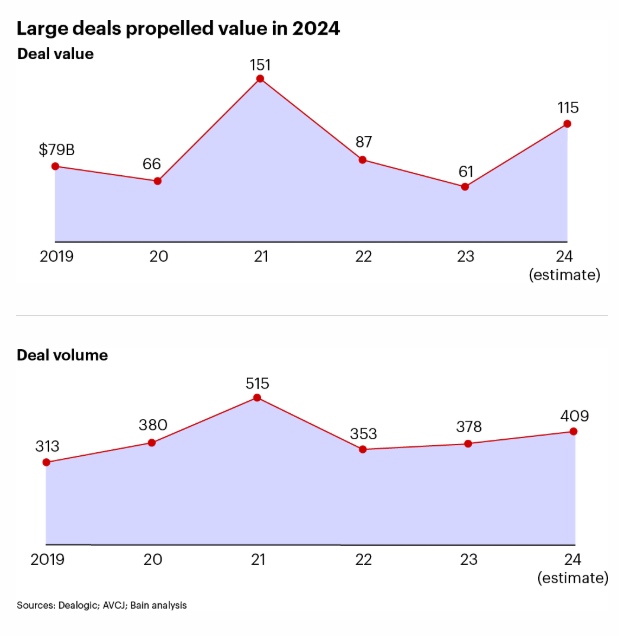

The healthcare industry has also seen large growth in private equity deal value and volume since 2019.

While healthcare deal value peaked at $151 billion in 2021, 2024 was also a very strong year, with $115 billion in value:

.

Source: Bain & Company

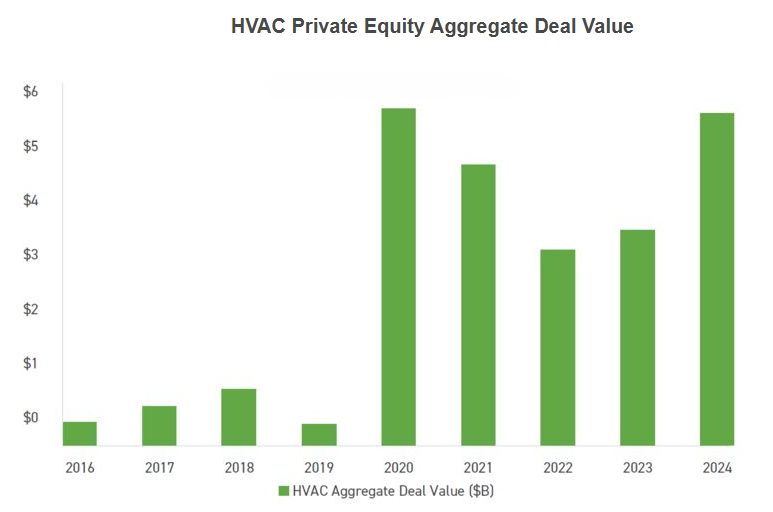

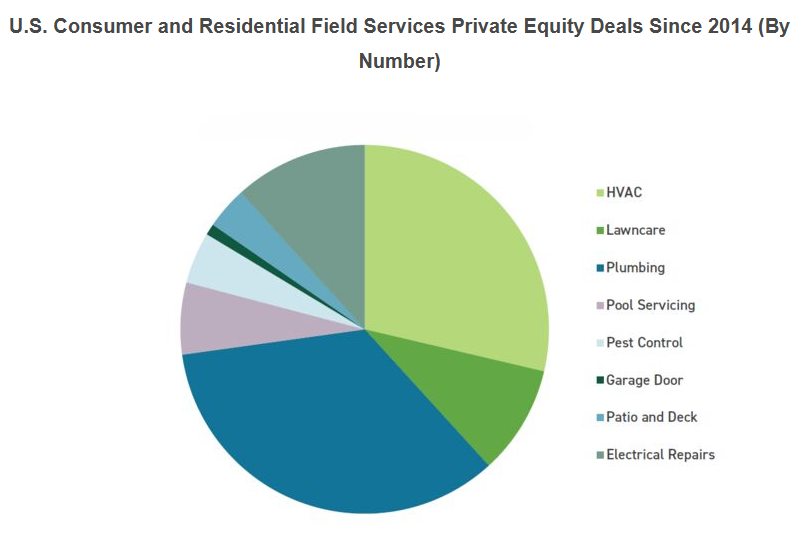

The services industry has seen exponential growth, as more firms implement roll-up strategies.

This has been seen in sectors like HVAC services, where private equity deal value exploded from 2019 to 2020, and continued through 2024:

Source: Cherry Bekaert

Private equity activity in other areas of service like plumbing and lawncare has also grown in recent years:

Source: Cherry Bekaert

Overall, many sectors have seen growth as overall private market value grows, headlined by technology and healthcare. Strategies like services roll ups have grown in popularity, and been able to provide outsized returns, due to their strong cashflows and opportunities for increased productivity.

The advent of generative AI should provide many more opportunities for investors in the tech space, and super-charge other strategies like services roll ups, which are prime for the productivity increases provided by AI.

How Finalis Can Help

In an increasingly fragmented market, solid deals can be difficult to source.

Through the Finalis platform, you can gain access to over 2,000 ongoing deals representing a total of over $100 billion in value, aligned to your own mandates.

As competition over deals heats up, and more investors get involved in private markets, closing deals efficiently is important. With Finalis’s automated compliance tools, you can ensure a deal never falls through because of regulatory red tape.

Using the Finalis platform, you can ensure you’re ready to capitalize on the next big trend.

Join Us

We recently launched a new program centered specifically around capital allocators, which will provide you:

- Curated investment opportunities from boutique bankers

- Vetted deals with structured financials

- Pre-screened counter parties

Through Finalis, you gain access to a network of over 330 trusted investment banks, saving you the hassle of finding trusted advisors.

You can access the platform with no upfront costs, so you can get started without commitment.

Joining Finalis is easy, and our onboarding process is often completed within the same day.

Get started today on our website

Contact our Capital Markets & Partnerships Director Nicanor Draghi at capital.markets@finalis.com for more information.