Introduction

Dry powder is reaching extraordinary levels, with estimates pinning the amount over $2 trillion globally across private equity, venture capital, and other private funds.

This level of capital presents an opportunity to reignite movement in the private markets, potentially yielding massive returns. However, many may still be holding back due to a variety of mitigating factors.

Following an explosion in dealmaking during 2021, there’s been a significant slowdown due to a grab bag of headwinds: rising interest rates, volatile markets, geopolitical tensions, and trade war concerns.

The slowdown has certainly not been equal between industries, and sectors that experienced the greatest declines could provide outsized opportunities as markets thaw and confidence returns.

Let’s examine what led to this treasure trove of stale capital and what allocators should be taking into consideration as sentiment turns around.

M&A Deal Values

Following the post-pandemic boom, M&A deal value greatly declined in 2022 and 2023. In the United States, total deal value fell 53.81% when comparing H1 2021 and H2 2022, from $1.388 trillion to $641 billion.

Source: PwC

Following this crash, deal value remained relatively stagnant in the U.S., staying within the $600-700 billion range through H2 2024.

On the global front, a similar trend was seen, with deal volume falling 47.42% when comparing H1 2021 and H2 2022, from $2.68 trillion to $1.41 trillion. Similar to the U.S., global deal value remained relatively stagnant through H2 2024.

Source: PwC

A recent report looking only at global buyouts shows a similar decline, but a greater climb coming out of 2023. Total investment value fell 56.18% when comparing 2021 to 2023, from $1 trillion to $438 billion.

From 2023 to 2024, however, global buyout investment value recovered 37.34%, from $438 billion to $602 billion.

Source: Bain Capital

In any case, M&A deal activity fell sharply from the peak in 2021, and has not yet fully returned. This has caused many to hold onto assets longer than desired and retreat from deploying capital at a greater scale.

Macroeconomic Factors

A main driver in falling activity was heightened interest rates by central banks, which was seen broadly across the globe.

In attempts to recover from the COVID-19 pandemic, many central banks provided large amounts of economic stimulus, leading to high inflation. The heightened interest rates that resulted made strategies like leveraged buyouts much less enticing.

At the beginning of 2022, the federal funds rate in the U.S. was just 0.25%. By mid-2023, rates had reached their peak of 5.5%.

However, rates began to soften in 2024, which helped to reduce the buyer-seller valuation gap that began in 2022.

Confidence in interest rates continuing to fall, along with the election of U.S. President Donald Trump, spurred a more rosy outlook heading into 2025.

This improved outlook faced some early challenges though, as the trade war concerns that followed created a great deal of uncertainty in markets.

The S&P 500 fell nearly 20% in the span of a couple months during 1H 2025, cratering investor confidence. This created chaos in dealmaking processes and many transactions may have been put on hold. A recent survey found that 30% of companies had paused or revisited deals in response to trade uncertainty.

As trade negotiations come along, some investor confidence has begun to return. This certainly presented itself in the M&A space, with deal value jumping 39% from April to May 2025 (among deals valued over $100 million).

The M&A Slowdown Summarized

While the slowdown was certainly real, especially in headline data, it was not a total freeze. High value transactions were still being discussed, and closing, even at the absolute height of uncertainty. A recent survey showed 51% of companies are still actively pursuing deals.

Many companies have become more selective in the transactions they took into consideration, focusing on deals that are core to their business. “The companies being sought after cut across all sectors and have a consistent track record, strong management and a well-supported growth plan,” according to a PwC report.

In 2025, fewer deals have been getting done, but those that are tend to be higher-value transactions. Total global deal count fell 9% in 1H 2025 compared to 1H 2024, however, total deal value is up 15%.

In other words, the slowdown is real in terms of breadth of activity, but it has been somewhat overblown if one assumes all deals came to a grinding halt.

As conditions continue to stabilize, many analysts expect the M&A environment to rebound further throughout 2025 and 2026, pending any wildcard crises. While a rebound will mean more movement, companies and investors may continue to be more selective in the deals they entertain.

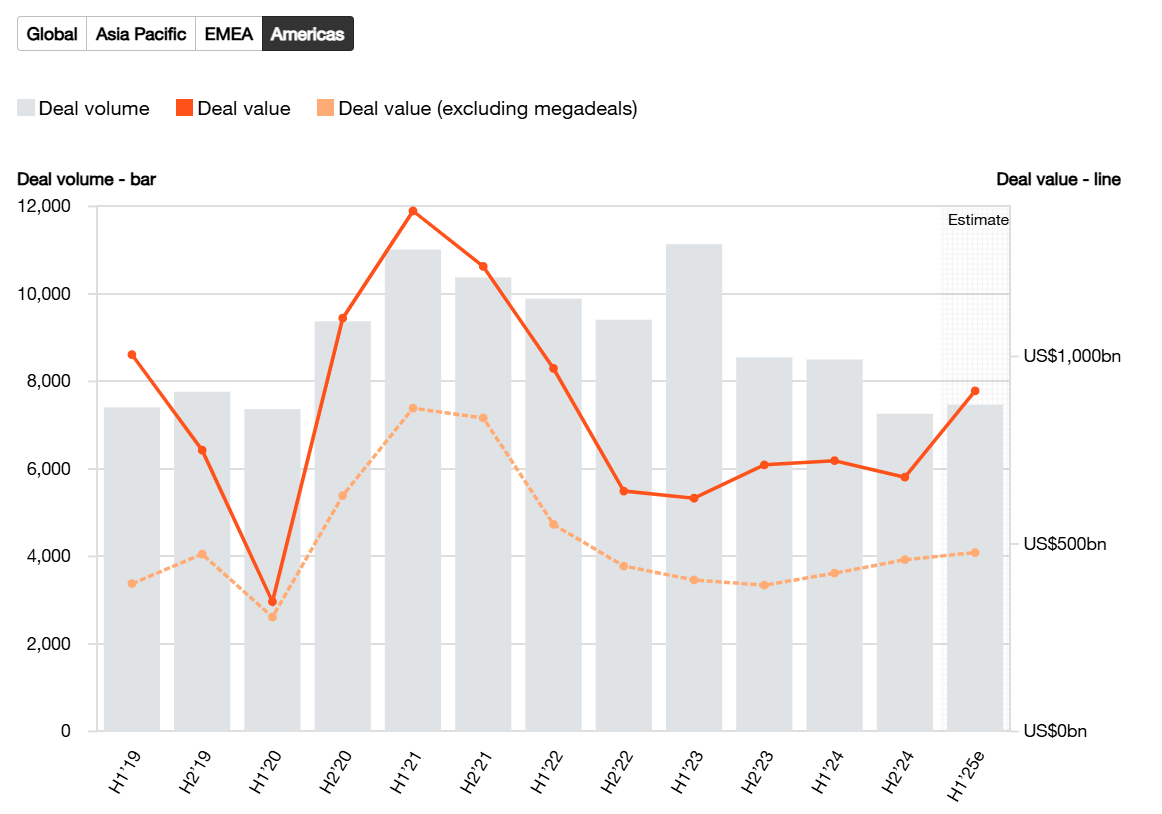

Rebound By Region

The rebound has played out slightly differently across international markets, but substantial global growth is ongoing.

Looking at deal value in 1H 2025 compared to 1H 2024, the Americas grew 26%, fueled by an increase in deals valued over $1 billion.

In Europe, deal values have declined 7%, resulting from a drop in megadeals completed in the UK. This could change in the second half of the year though, as Europe has become a very attractive option for diversification amid U.S. uncertainty.

In Asia, deal values grew 14%, boosted by two megadeals in Japan and robust mid-market activity in India.

Venture Capital

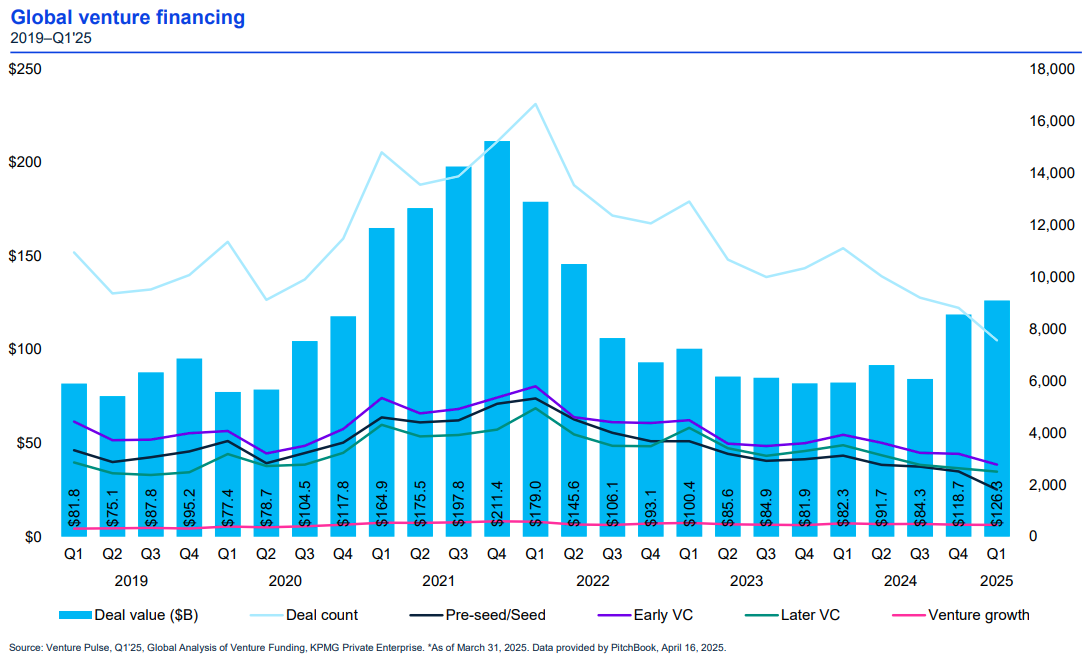

Venture capital has experienced a similar slowdown to M&A, following record activity in 2021.

In the U.S., venture financing activity bottomed out at $35.4 billion total value in Q3 2023, a steep 64.9% decline from its peak of $101 billion total value in Q4 2021.

Source: KPMG

Global venture financing saw a similar slowdown on a similar timeline to the U.S., with deal value bottoming out in Q4 2023 at $81.9 billion, an 83.3% decline from the peak of $211.4 billion in Q4 2021.

Source: KPMG

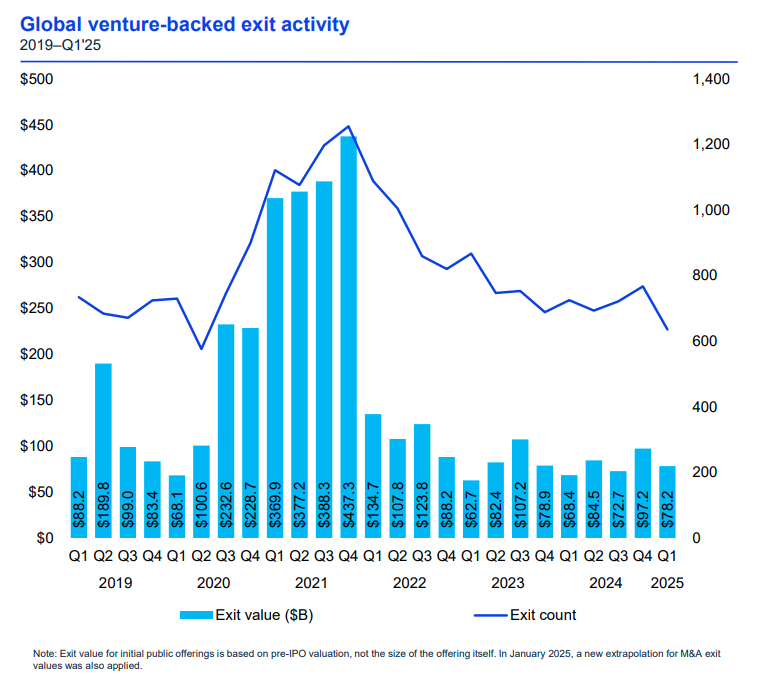

As public markets declined in 2022, IPOs became significantly less attractive, which had a profound impact on venture outlook, slamming the door shut on one of the most popular exit opportunities for funds.

Global exit value in the venture space bottomed out at $62.7 billion in Q1 2023, a shocking 85.66% decline from its peak of $437.4 billion in Q4 2021.

Since then, exit value has seen slight gains, but is still nowhere near the peaks seen throughout 2021.

Source: KPMG

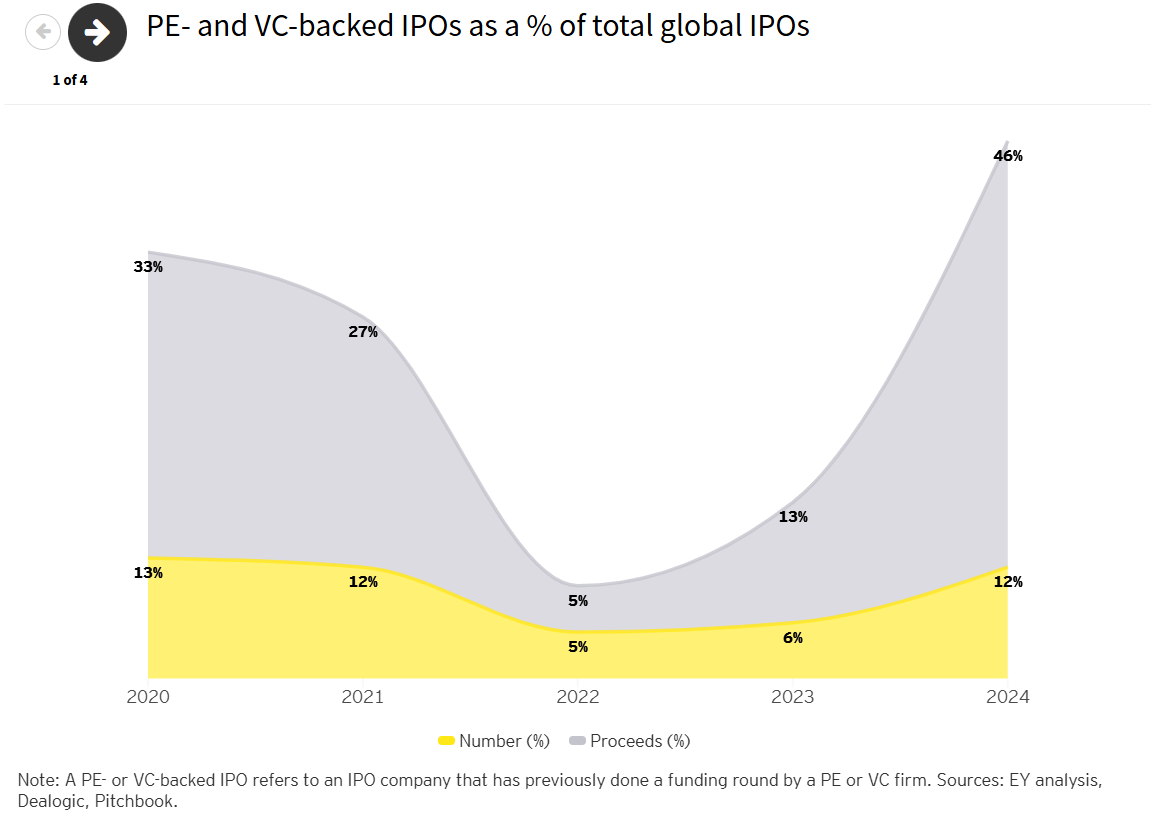

A decline in IPO activity has been a major contributing factor in the mounting size of stale capital, as some began holding out on going public, waiting for higher valuations. The percentage of global IPOs backed by private equity and venture declined from 12% in 2021 to 5% in 2022.

The overall proceeds of IPOs backed by PE and venture plummeted as well, from 27% of total global IPO proceeds in 2021 to just 5% in 2022.

Source: EY

The IPO market has shown signs of thawing. From the 2022 lows, total share of global IPO proceeds by PE and venture bumped up to 13% in 2023, and rocketed to 46% in 2024.

Recovering sentiment in 2025 has continued lifting spirits in the IPO market. So far, 95 companies have listed on U.S. exchanges, creating proceeds of $15.6 billion as of mid-June. Total listings are up 30% from the same period in 2024, returning IPOs as a viable exit opportunity for allocators.

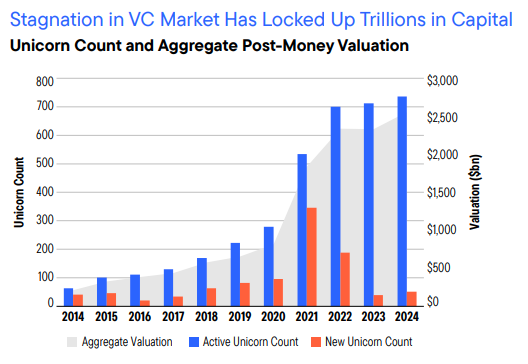

Another headwind faced by venture since 2021 is a significant decline in new “unicorn” opportunities, or companies valued over $1 billion.

Source: Franklin Templeton

This issue has been compounded by declining exit opportunities for existing unicorns since the 2021 boom, locking up capital for venture firms. However, as the IPO market begins to heat back up, this could begin to resolve.

The artificial intelligence race should also provide tailwinds for venture in the coming years, as numerous companies and nations battle for dominance. AI has propelled venture activity in the U.S., helping it attain its position as the top destination in Q1 2025, even amid the ongoing uncertainty.

A recent $40 billion raise for OpenAI and $4.5 billion raise for Anthropic contributed to the U.S.’s top position in total VC funding for the first quarter of the year.

Europe came in second for total VC funding during Q1 2025, headlined by a $2.5 billion raise for Binance.

Overall, venture has been on a similar trajectory to M&A in recent years, and should benefit from a combination of returning investor confidence, resolving uncertainty, and falling interest rates throughout the remainder of 2025 and 2026.

Total venture financing saw significant growth in Q4 2024 and Q1 2025 when looking at both the U.S. and globally, and viable exit opportunities should continue becoming more common.

Fundraising

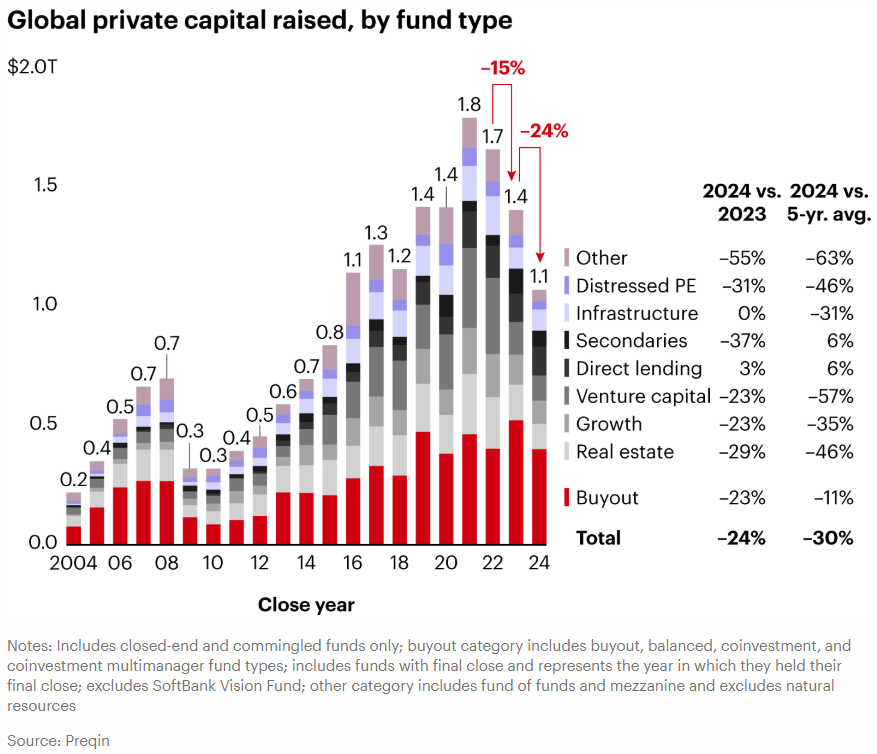

Overall private fundraising has also declined in recent years, commensurate with the drop in deal activity from 2021 peaks.

Peaking at $1.8 trillion in 2021, private fundraising between all sectors fell for three straight years, bottoming out in 2024 at $1.1 trillion, a 38.8% decline.

Notably, buyout fundraising declined by 23% in 2024 when compared with 2023, and was down 11% when compared to the 5 year average.

While buyout fundraising hit lows in 2024, 2023 was a record year, even higher when overall raises across all sectors peaked.

2024’s decline in buyout fundraising was headlined by a drop of 34% in North America, with a relatively flat value in Europe, and a rise of 13% in Asia.

This suggests that U.S. investors, facing the denominator effect (with public markets down in 2022-23), and a large amount of undrawn commitments, pulled back sharply on newer ones.

Source: Bain & Company

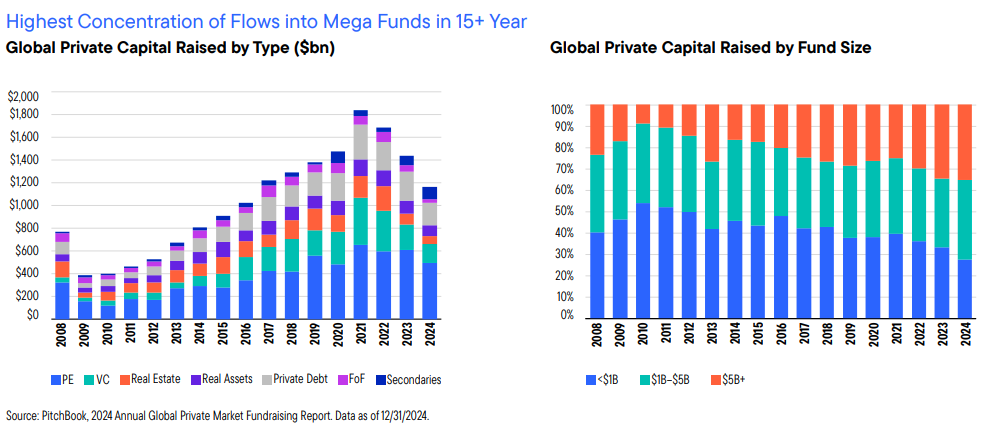

Another defining fundraising trend in recent years is a concentration of capital. LPs have displayed a flight to safety by committing primarily to the most established funds, while smaller or newer managers are struggling.

Short-term treasury bond yields have also been attractive, with the latest 3-month and 6-month yielding over 4%. High short-term bond yields have allowed LPs to safely grow their stash, making longer-term commitments less desirable for the time being.

In the first half of 2024, the majority of capital went to mega-funds, reaching the highest concentration in 15 years.

This has led to a bifurcated fundraising market: the top-quartile firms often close oversubscribed funds, while lower-tier GPs face prolonged fundraising timelines.

By 2024, the average time to close a buyout fund had stretched to around 20 months, nearly double the pre-pandemic norm.

Source: Franklin Templeton

Overall, the slower pace of capital recycling, due to lower exit values, has exacerbated the issues in fundraising. LPs have less cash coming back and tighter budgets for new commitments as a result.

With lower commitments, LPs have been trying to mitigate risks of new ones by concentrating capital into the biggest and most established funds, while smaller funds face difficulties.

Slowdown By Sector

Slowdowns in dealmaking have been more severe in some sectors than others.

According to PwC data, when excluding megadeals, several sectors declined in both deal value and volume globally when comparing H1 2024 to H1 2025:

- Auto, engineering and manufacturing (-5.5% volume, -8.9% value)

- Hospitality and leisure (-11.1% volume, -19.6% value)

- Entertainment and media (-15.6% volume, -29% value)

- Pharmaceuticals (-19.1% volume, -33.6% value)

- Mining and metals (-6.3% volume, -6.3% value)

- Banking and capital markets (-3.9% volume, -13.2% value)

Tariff vulnerability played a large role in decreasing value and volume for some sectors, as both auto and pharmaceuticals are heavily exposed to potential trade barriers.

Pharmaceuticals also experienced some concerns around new policy in the U.S., including uncertainty around drug pricing, and further scrutiny towards pharmaceutical companies,

However, when including megadeals, some of these sectors saw large gains in deal value, including entertainment and media, which had a 110.9% gain.

While megadeals can’t be counted on every quarter, it does give some gas to the narrative that companies are simply becoming more selective about the deals they pursue, preferring high-value ones.

Those most exposed to tariffs and uncertainty, like auto and pharmaceuticals, saw drops in both value and volume, even with megadeals included.

Surprisingly, despite their exposure to trade barriers, retail and consumer saw a climb in deal value during 1H 2025 when compared with 1H 2024 (33.8% excluding megadeals, 46.1% including).

There were, however, declines in volume for the sector. This further suggests companies preference towards high-value deals as of recent.

Some sectors have remained more resilient in the face of uncertainty, PwC data showed that these sectors grew in both volume and value globally, when excluding megadeals, during 1H 2025 in comparison to 1H 2024:

- Aerospace and defense (+10.2% volume, +20.5% value)

- Power and utilities (+1.9% volume, +3.1% value)

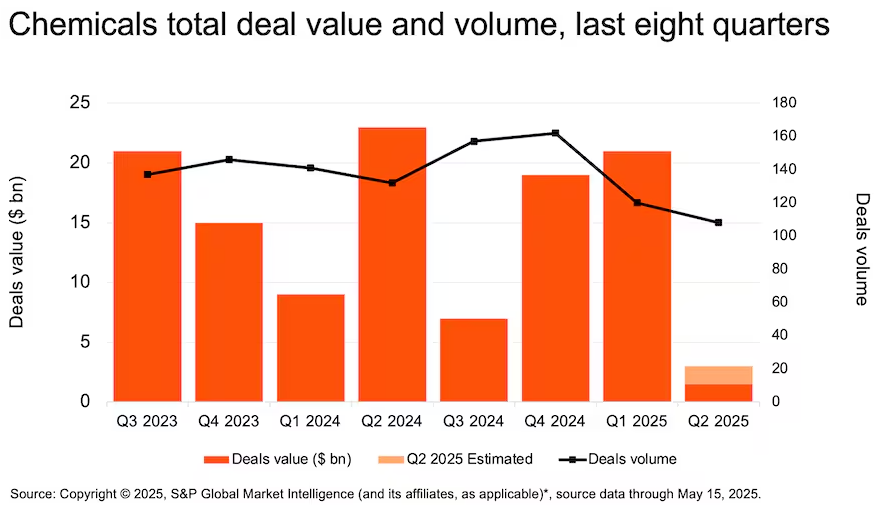

- Chemicals (+6% volume, 36.8% value)

When including megadeals, the sectors which both grew in volume and value globally when comparing 1H 2024 and 1H 2025 were the same, with greater boosts in value:

- Aerospace and defense (+151.9% value)

- Chemicals (+162.3% value)

- Power and utilities (+87.6% value)

Aerospace and defense received uncertainty as a tailwind, instead of a headwind, as some nations looked to bolster their domestic defense capabilities due to mixed U.S. messaging.

Power and utilities are set to continue performing highly, as energy demand skyrockets from AI data centers.

High performance in chemicals during 1H 2025 was mostly contributed to by momentum from Q4 2024 and transactions in Q1 2025, as dealmaking in the sector slowed significantly during Q2 2025.

Source: PwC

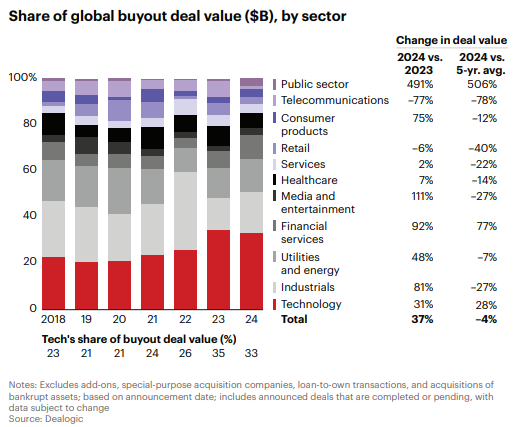

When looking at global buyout value share by sector from 2021-2024, technology was by far the biggest winner, representing 33% of total value in 2024, and an average of 27.7% over a 5-year period.

In fact, tech’s overall share of global buyout value actually grew from 2021 over the following years through 2024, although there was a small dip when comparing 2023 and 2024.

Source: Bain & Company

Sectors that underperformed were much greater than those that overperformed when comparing 1H 2024 and 1H 2025, underscoring the more cautious dealmaking environment.

However, many analysts expect a recovery over the remainder of 2025 and 2026, which should bring gains in volume and value to several sectors.

As regulatory and trade policy issues become more clear, affected sectors like pharmaceuticals and auto could see greater recoveries.

Timing of Deployment

Broadly, caution still persists, but is starting to diminish. In 2025, lots of capital is still effectively on the sidelines waiting for the right moment. The fact that global deal volumes remain down year-over-year shows that many investors are selectively holding back, and are not doing as many deals as before.

However, it’s been said that uncertainty may be a new “permanent state” according to a report by PwC , so holding back indefinitely waiting for the perfect moment is not a viable strategy.

There are several reasons to believe that dry powder could be set to be deployed en masse over the coming years:

For one, declining interest rates should be a huge boon for dealmaking, as borrowing money to complete leveraged buyouts will become more enticing. Investors are now pricing in a 62.1% chance of a rate cut by September 2025.

Conditions in exit markets are also starting to improve. Several successful IPOs have been seen so far in 2025 and the secondary market has started to pick up pace with several large deals by the NYC pension system and Yale’s endowment.

The valuation gap is beginning to close, bringing prices to a more reasonable level for buyers and helping sellers offload assets faster. More reasonable valuations have also played a role in heating up the IPO market.

This year, there have been 101 IPOs, an increase of 44.3% from the same period in 2024.

Additionally, fund managers are facing pressure to garner more exits. In 2024, average exit times reached a record high of 8.5 years, more than double the time of 4.1 years seen in 2007.

Strategic M&A should also pick up in the coming years, especially in the tech and energy sectors, as companies race to release and scale more powerful AI models. Corporations are sitting on an immense amount of cash on their balance sheets, with estimates as high as $7.5 trillion. This stash will allow them to make more growth-focused investments, including acquisitions.

Overall, these factors combine to suggest brighter days ahead for private markets, especially with the record amount of dry powder in waiting.

Why 2025 Is the Moment

- Dry powder has reached historic levels with an estimated $2 trillion globally

- Investors are getting used to volatility as the “new normal” and will adapt to deploying capital in more uncertain conditions

- Interest rates are set to begin declining, with 2 rate cuts in the U.S. expected before year-end, and potentially more if inflation remains tame

- Exit markets are beginning to pick up speed, with large secondaries deals and greater activity in the IPO market than in 2024

- Valuations are becoming more reasonable, as 2021 activity created overestimations that sellers are adjusting to

- Pressure from LPs for GPs to achieve more exits is picking up

- Companies are sitting on large piles of cash that can be used to make strategic, growth-focused investments in the M&A market

- AI is creating new value in the tech space as new use cases are discovered and the race for more powerful models picks up speed

How Finalis Can Help

While investors look to deploy dry capital at scale, sourcing the right opportunities will be important to put money in the right places.

Through our platform, gain access to over 2,000 ongoing deals representing a total of over $100 billion in value, aligned to your own mandates.

Private markets can be tough to navigate, but as activity picks up, Finalis can ensure you’re ready to put money back on the market with the best available opportunities at highly efficient speeds.

Our platform enables deal closures in just 2–3 months on average — dramatically faster than the traditional private market exit cycle.

Using the power of the Finalis platform, you can ensure you’re prepared to capitalize as sentiment turns around within private markets over the remainder of the year.

Join Us

We recently launched a new program centered specifically around capital allocators, which will provide you:

- Curated investment opportunities from boutique bankers

- Vetted deals with structured financials

- Pre-screened counter parties

Through Finalis, you gain access to a network of over 330 trusted investment banks, saving you the hassle of finding trusted advisors.

We’re currently offering a no-cost trial period for institutional investors, so you can get started without commitment.

Joining Finalis is easy, and our onboarding process is often completed within the same day.

Get started today on our website

Contact our Capital Markets & Partnerships Director Nicanor Draghi at nicanor.draghi@finalis.com for more information.

.jpg)